Structure of the Study Material

- Overview of AS-1 and Fundamental Accounting Assumptions

- Detailed Explanation of Each Assumption

- Comparison with Other Accounting Concepts

- Answer to the Provided Question

- Common Misconceptions and Clarifications

- Practice Questions with Explanations

1. Overview of AS-1 and Fundamental Accounting Assumptions

Accounting Standard-1 (AS-1), titled “Disclosure of Accounting Policies,” is a foundational standard under Indian GAAP that governs the preparation and presentation of financial statements. It mandates the disclosure of significant accounting policies adopted by an entity to ensure transparency and comparability. AS-1 identifies three fundamental accounting assumptions that underlie the preparation of financial statements unless explicitly stated otherwise. These assumptions are critical as they form the basis for accounting practices and are presumed to be followed unless a deviation is disclosed.

The three fundamental accounting assumptions as per AS-1 are:

- Going Concern

- Consistency

- Accrual

These assumptions ensure that financial statements reflect a standardized approach to recording and reporting financial transactions, facilitating stakeholder decision-making.

2. Detailed Explanation of Each Assumption

a. Going Concern

- Definition: The financial statements are prepared on the assumption that the entity will continue its operations for the foreseeable future without the need to liquidate its assets or cease operations.

- Implication: Assets are valued at historical cost (or other relevant bases like fair value) rather than liquidation value, and liabilities are expected to be settled in the normal course of business.

- Example: A company records machinery at ₹10,00,000 with depreciation over 10 years, assuming it will use the asset for its intended purpose rather than selling it immediately.

- Rationale: This assumption justifies long-term investments, deferred expenses, and the matching of costs with revenues over time.

- Exception: If the entity is facing insolvency or plans to shut down, this assumption does not hold, and financial statements may reflect liquidation values.

b. Consistency

- Definition: Accounting policies and methods are applied consistently from one period to another to ensure comparability of financial statements over time.

- Implication: Changes in accounting policies (e.g., method of depreciation from straight-line to written-down value) are allowed only if required by statute, for better presentation, or for compliance with new standards, and must be disclosed with their impact.

- Example: If a company uses the straight-line method for depreciation in Year 1, it should continue using it in Year 2 unless a valid reason for change is disclosed.

- Rationale: Consistency enhances the reliability of financial analysis, enabling users to compare performance across periods.

- Exception: Changes due to new accounting standards or improved accuracy are permitted but require retrospective application and disclosure.

c. Accrual

- Definition: Revenues and expenses are recognized when they are earned or incurred, not when cash is received or paid. This is also known as the accrual basis of accounting.

- Implication: Financial statements reflect economic activities of a period, regardless of cash flow timing. For example, sales on credit are recorded as revenue when the sale occurs, not when payment is received.

- Example: A company delivers goods worth ₹50,000 in March but receives payment in April. Under the accrual basis, revenue is recognized in March.

- Rationale: This assumption aligns income and expenses with the period they relate to, providing a true and fair view of financial performance.

- Exception: Small entities or specific industries may use the cash basis, but this deviates from AS-1’s assumption and must be disclosed.

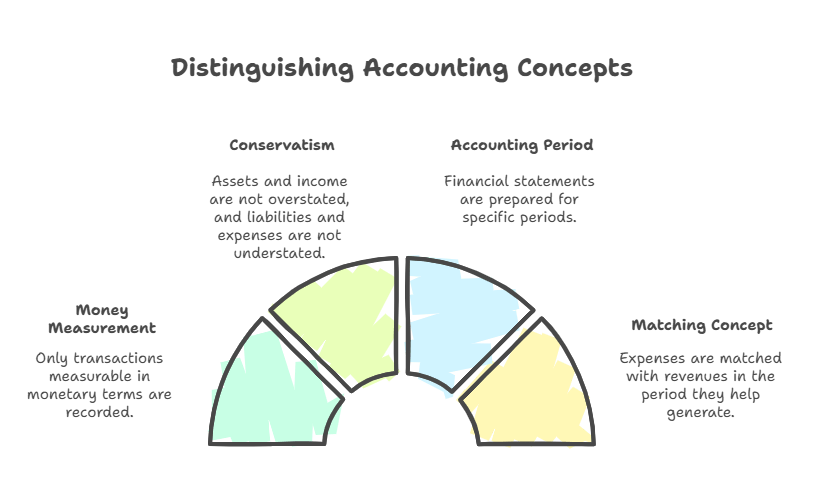

3. Comparison with Other Accounting Concepts

To avoid confusion, it’s important to distinguish the fundamental accounting assumptions from other accounting principles or concepts often tested in exams:

- Money Measurement: Only transactions measurable in monetary terms are recorded. While crucial, it is a concept, not a fundamental assumption under AS-1.

- Conservatism (Prudence): Assets and income are not overstated, and liabilities and expenses are not understated. This is a principle guiding accounting estimates but not a fundamental assumption.

- Accounting Period: Financial statements are prepared for specific periods (e.g., annually). This is a convention, not an assumption under AS-1.

- Matching Concept: Expenses are matched with revenues in the period they help generate. This is derived from the accrual assumption but is not listed separately in AS-1.

4. Answer to the UPSC APFC 2023 Question

Question: According to Accounting Standard-1, which of the following are the fundamental accounting assumptions?

(a) Going Concern, Consistency, Accrual

(b) Going Concern, Money Measurement, Conservatism

(c) Going Concern, Consistency, Conservatism

(d) Going Concern, Accounting Period, Accrual

Correct Answer: (a) Going Concern, Consistency, Accrual

Explanation:

As per AS-1, the fundamental accounting assumptions are explicitly defined as Going Concern, Consistency, and Accrual. These assumptions underpin the preparation of financial statements and are presumed to be followed unless stated otherwise.

- Option (b) includes Money Measurement and Conservatism, which are accounting concepts/principles, not fundamental assumptions.

- Option (c) includes Conservatism, which is incorrect for the same reason.

- Option (d) includes Accounting Period, which is an accounting convention, not a fundamental assumption.

Thus, option (a) is the only correct choice.

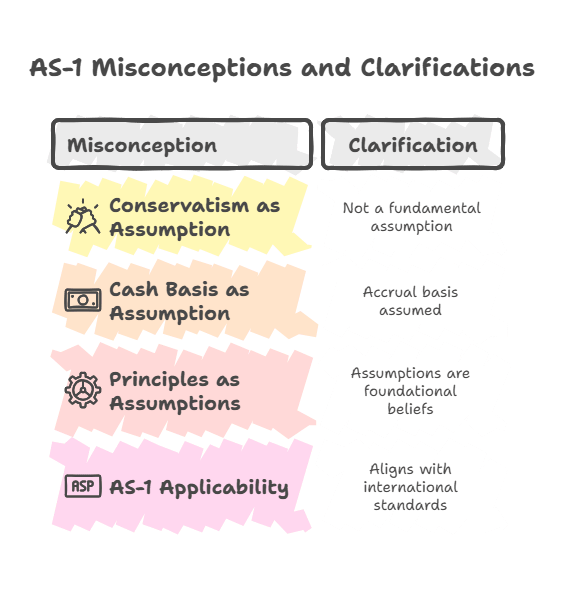

5. Common Misconceptions and Clarifications

- Misconception 1: Conservatism is a fundamental assumption.

Clarification: Conservatism (prudence) is a principle under AS-1 that influences accounting judgments but is not listed as a fundamental assumption. It is emphasized in standards like Ind AS 37 for provisions but not in AS-1’s core assumptions. - Misconception 2: Cash basis is an alternative assumption under AS-1.

Clarification: AS-1 assumes the accrual basis. The cash basis is a deviation and must be disclosed if adopted. - Misconception 3: All accounting principles are assumptions.

Clarification: Assumptions (like going concern) are foundational beliefs taken for granted unless contradicted, while principles (like conservatism) guide specific accounting treatments. - Misconception 4: AS-1 applies only to Indian entities.

Clarification: While AS-1 is part of Indian GAAP, its principles align with international standards like IAS 1, making it relevant for global accounting contexts.

6. Practice Questions with Explanations

To ensure mastery of similar questions, practice the following:

- Question: Which of the following is NOT a fundamental accounting assumption under AS-1?

(a) Going Concern

(b) Consistency

(c) Accrual

(d) Conservatism

Answer: (d) Conservatism

Explanation: AS-1 lists Going Concern, Consistency, and Accrual as fundamental assumptions. Conservatism is a principle, not an assumption. - Question: A company prepares its financial statements assuming it will operate for the next 10 years. This reflects which assumption?

(a) Consistency

(b) Accrual

(c) Going Concern

(d) Money Measurement

Answer: (c) Going Concern

Explanation: The assumption that the entity will continue operations for the foreseeable future is the Going Concern assumption. - Question: If a company changes its depreciation method from straight-line to written-down value, which assumption is affected?

(a) Going Concern

(b) Consistency

(c) Accrual

(d) None of the above

Answer: (b) Consistency

Explanation: A change in accounting policy (like depreciation method) impacts the Consistency assumption, requiring disclosure of the change and its effect. - Question: Recording sales revenue when goods are delivered, not when payment is received, is based on which assumption?

(a) Going Concern

(b) Consistency

(c) Accrual

(d) Conservatism

Answer: (c) Accrual

Explanation: The Accrual assumption recognizes revenues when earned, regardless of cash receipt. - Question: Which of the following combinations includes a fundamental accounting assumption and an accounting principle?

(a) Going Concern and Money Measurement

(b) Consistency and Conservatism

(c) Accrual and Accounting Period

(d) Going Concern and Consistency

Answer: (b) Consistency and Conservatism

Explanation: Consistency is a fundamental assumption under AS-1, while Conservatism is an accounting principle. Other options either include two assumptions or non-assumptions. - Question: If an entity is under liquidation, which fundamental assumption is violated?

(a) Consistency

(b) Accrual

(c) Going Concern

(d) None of the above

Answer: (c) Going Concern

Explanation: Liquidation contradicts the Going Concern assumption, as the entity is not expected to continue operations.

Leave a comment