1. Microeconomics vs. Macroeconomics

Overview

Economics is broadly divided into two main branches: microeconomics and macroeconomics. These branches help us analyze economic phenomena at different scales. Demand and supply are core concepts primarily studied in microeconomics, but they have implications for macroeconomic issues like inflation and unemployment.

Key Differences

Use the table below to compare the two branches:

| Aspect | Microeconomics | Macroeconomics |

|---|---|---|

| Focus | Individual units (e.g., consumers, firms, markets) | Aggregate economy (e.g., national output, overall price levels) |

| Key Topics | Demand and supply, pricing, consumer behavior, competition | GDP, inflation, unemployment, fiscal and monetary policy |

| Scale | Small-scale decisions (e.g., how a firm sets prices) | Large-scale phenomena (e.g., national economic growth) |

| Examples | How a coffee shop decides how much coffee to produce based on customer demand | How government spending affects overall employment in the country |

| Tools/Analysis | Supply-demand curves, elasticity, market structures | Aggregate demand-supply models, business cycles |

Detailed Explanation

- Microeconomics: This branch examines how individuals and businesses make decisions to allocate limited resources. It assumes “ceteris paribus” (all other things being equal) to isolate variables. For instance, microeconomics would analyze how a change in the price of apples affects consumer purchases in a local market.

- Macroeconomics: This deals with the economy as a whole, focusing on broad indicators like total output (GDP), inflation rates, and unemployment. It considers interconnections across the economy, such as how a recession impacts multiple industries.

Demand and supply models originate in microeconomics but aggregate to form macroeconomic concepts like aggregate demand (total demand in the economy) and aggregate supply (total production).

Why It Matters

Understanding the distinction helps contextualize demand and supply: In microeconomics, they explain individual market behaviors, while in macroeconomics, they scale up to explain national trends.

Review Questions

- What is the primary difference in scale between micro and macroeconomics?

- Give an example of a microeconomic question related to demand and supply.

2. Basics of Demand

Definition

Demand refers to the quantity of a good or service that consumers are willing and able to purchase at various price levels over a specific period, assuming other factors remain constant. It reflects consumer desire backed by purchasing power.

The Law of Demand

The law of demand states that, all else equal, as the price of a good decreases, the quantity demanded increases, and vice versa. This inverse relationship occurs due to:

- Substitution effect: Consumers switch to cheaper alternatives.

- Income effect: Lower prices effectively increase purchasing power.

- Diminishing marginal utility: Additional units provide less satisfaction, so consumers buy more only at lower prices.

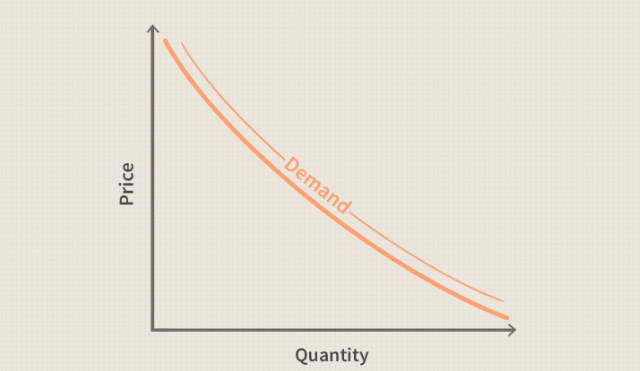

Demand Schedule and Curve

A demand schedule is a table showing the quantity demanded at different prices. For example, for smartphones:

| Price per Smartphone ($) | Quantity Demanded (units per month) |

|---|---|

| 1000 | 100 |

| 800 | 200 |

| 600 | 400 |

| 400 | 700 |

| 200 | 1200 |

The demand curve is a graphical representation of the demand schedule, sloping downward from left to right.

Determinants of Demand (Shifters)

Demand can shift due to non-price factors, causing the entire curve to move left (decrease) or right (increase):

- Income: Normal goods (demand increases with income, e.g., cars); Inferior goods (demand decreases with income, e.g., generic brands).

- Prices of related goods: Substitutes (e.g., tea and coffee—if coffee price rises, tea demand increases); Complements (e.g., printers and ink—if printer price falls, ink demand increases).

- Tastes and preferences: Changes due to trends, advertising, or cultural shifts.

- Expectations: If consumers expect future price increases, current demand rises.

- Number of buyers: Population growth increases demand.

- Other factors: Government policies, seasons, or demographics.

Quantity Demanded vs. Demand

- Change in quantity demanded: Movement along the curve due to price changes.

- Change in demand: Shift of the entire curve due to determinants.

Examples

- If a new health study promotes apples, demand for apples shifts right.

- During a sale, quantity demanded for clothes increases (movement along the curve).

Review Questions

- Explain the law of demand with an example.

- What causes a shift in the demand curve versus a movement along it?

3. Basics of Supply

Definition

Supply is the quantity of a good or service that producers are willing and able to offer for sale at various price levels over a specific period, assuming other factors remain constant. It reflects producer incentives.

The Law of Supply

The law of supply states that, all else equal, as the price of a good increases, the quantity supplied increases, and vice versa. This positive relationship occurs because higher prices mean higher profits, encouraging more production.

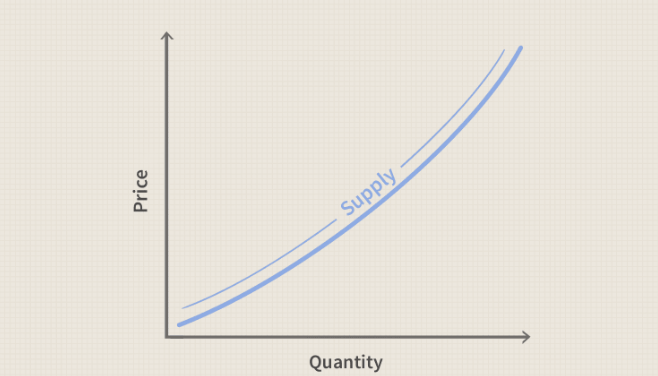

Supply Schedule and Curve

A supply schedule lists quantities supplied at different prices. For example, for wheat (per farmer):

| Price per Bushel ($) | Quantity Supplied (bushels per month) |

|---|---|

| 2 | 100 |

| 3 | 200 |

| 4 | 400 |

| 5 | 700 |

| 6 | 1000 |

The supply curve graphs this, sloping upward from left to right.

Determinants of Supply (Shifters)

Supply shifts due to non-price factors, moving the curve left (decrease) or right (increase):

- Input costs: Lower costs (e.g., cheaper raw materials) increase supply.

- Technology: Improvements (e.g., automation) increase efficiency and supply.

- Prices of related goods: If alternative products become more profitable, supply of the current good decreases.

- Expectations: If producers expect higher future prices, current supply decreases.

- Number of sellers: More firms enter the market, increasing supply.

- Other factors: Government subsidies/taxes, weather (for agriculture), or regulations.

Quantity Supplied vs. Supply

- Change in quantity supplied: Movement along the curve due to price changes.

- Change in supply: Shift of the entire curve due to determinants.

Examples

- A technological breakthrough in solar panels shifts supply right (more panels at each price).

- Rising oil prices increase quantity supplied of oil (movement along the curve).

Review Questions

- Why does the supply curve slope upward?

- List two factors that could shift the supply curve to the left.

4. Market Equilibrium

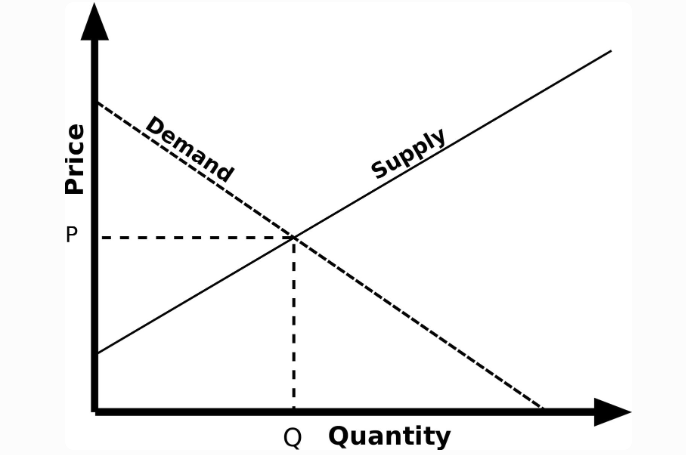

Definition

Market equilibrium occurs when the quantity demanded equals the quantity supplied at a specific price, known as the equilibrium price (P). The corresponding quantity is the equilibrium quantity (Q). At this point, there is no shortage or surplus—the market clears.

How Equilibrium is Achieved

Markets adjust through price signals:

- Surplus (excess supply): If price > P*, quantity supplied > demanded → prices fall to eliminate surplus.

- Shortage (excess demand): If price < P*, quantity demanded > supplied → prices rise to eliminate shortage.

In a free market, these adjustments lead to equilibrium without intervention.

Graphical Representation

Equilibrium is where the demand and supply curves intersect.

Changes in Equilibrium

- Demand shifts right: Higher P* and Q* (e.g., population boom increases housing demand).

- Demand shifts left: Lower P* and Q* (e.g., health scare reduces demand for a food item).

- Supply shifts right: Lower P* but higher Q* (e.g., subsidy on electric cars).

- Supply shifts left: Higher P* but lower Q* (e.g., natural disaster reduces crop supply).

- Simultaneous shifts: Outcomes depend on the magnitude (e.g., demand increases more than supply → higher P*).

Examples

- In the oil market: A geopolitical event reduces supply (shift left) → higher prices until new sources are found.

- Smartphone market: New features increase demand (shift right) → higher prices and production.

Why It Matters

Equilibrium explains resource allocation in markets and predicts responses to changes, forming the basis for policy analysis (e.g., price controls like ceilings or floors, which can cause inefficiencies).

Review Questions

- What happens if the market price is above equilibrium?

- Describe how a simultaneous increase in demand and decrease in supply affects equilibrium.

Leave a comment